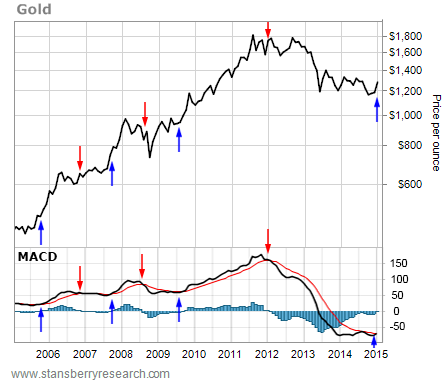

Taking Steve Saville's analysis of the "1970s" gold bull however he would show the real move in the miners starting in the 1960s even while the metal price was fixed.

Very junior discovery activity seems out of bounds (similarly even "GLDX explorers ETF holdings" are mainly developers of well explored and defined deposits, so really just taking the producing aspect out of GDXJ).

- "Why invest in junior miners? -"High-value discoveries and mine development can create enormous upside potential" ..........But......."The Index methodology tends to favor junior and intermediate producers versus early stage exploration companies whose historical success rate is low."

| COMPANY | TICKER | Weight % |

| B2Gold Corp | BTO CN | 7.71% |

| Centerra Gold Inc | CG CN | 6.46% |

| First Majestic Silver Corp | AG US | 6.08% |

| Hecla Mining Co | HL US | 5.63% |

| Pan American Silver Corp | PAAS US | 5.60% |

| Alamos Gold Inc | AGI CN | 5.23% |

| Harmony Gold Mng-Spon ADR | HMY US | 4.23% |

| IAMGOLD Corp | IAG US | 4.16% |

| Primero Mining Corp | PPP US | 3.72% |

| OceanaGold Corp | OGC CN | 3.47% |

| Sandstorm Gold Ltd | SAND US | 3.41% |

| Aurico Gold Inc | AUQ US | 3.17% |

| Detour Gold Corp | DGC CN | 3.00% |

| Rio Alto Mining Ltd | RIO CN | 2.74% |

| China Gold International Res | CGG CN | 2.69% |

| Nevsun Resources Ltd | NSU CN | 2.65% |

| Alacer Gold Corp | ASR CN | 2.59% |

| Kirkland Lake Gold Inc | KGI CN | 2.57% |

| Lake Shore Gold Corp | LSG CN | 2.47% |

| Novagold Resources Inc | NG US | 2.26% |

| Argonaut Gold Inc | AR CN | 2.22% |

| Semafo Inc | SMF CN | 2.05% |

| Fortuna Silver Mines Inc | FSM US | 1.87% |

| Silver Standard Resources | SSRI US | 1.67% |

| Endeavour Silver Corp | EXK US | 1.55% |

| Dundee Precious Metals Inc | DPM CN | 1.47% |

| Torex Gold Resources Inc | TXG CN | 1.46% |

| Gold Resource Corp | GORO US | 1.37% |

| Pretium Resources Inc | PVG US | 1.22% |

| Rubicon Minerals Corp | RBY US | 1.04% |

| Premier Gold Mines Ltd | PG CN | 0.97% |

| Mag Silver Corp | MAG CN | 0.78% |

| Seabridge Gold Inc | SA US | 0.71% |

| Guyana Goldfields Inc | GUY CN | 0.66% |

| Asanko Gold Inc | AKG CN | 0.59% |

| Continental Gold Ltd | CNL CN | 0.53% |

While Finance Minister Carlos Leitao announced plans for the fund in June, Quebec’s legislature has yet to authorize its creation. Capital Mines Hydrocarbures should be able to support as many as 10 mining projects once it begins operating, Daoust said. “The raison d’etre of that fund is to make sure that at the end of the day, if the funding is complicated for the last 10 or 20 percent of a project, we will be there,” the minister said. “We can go to C$200 million, but normally we should not invest more than 10 or 15 percent of a project.”

But Newmont, the world’s No. 2 gold producer after Barrick, is likely to emerge a winner even if gold falls further. The Greenwood Village, Colo.–based company has sold assets and cut costs, reducing its break-even production price by about $200 in the past two years, to $1,002 an ounce.

Put all that together and it’s all happening now. You know what? There are a lot of weird things that I can’t really figure how it’s going to end. But quite frankly, my salvation here, my refuge, is in precious metals. It’s in gold and silver. So I’m very bullish on gold right now. I’m particularly bullish watching what’s happening to the gold price relative to the US dollar. I’m bullish on silver because silver will follow gold. Silver has always traded with gold...........This is the end of four years of really weak markets, in the metal space and in the resources space. So a lot of investors are bruised and bloodied. We’re starting the fifth year. If the tide is going out and there is a huge macro wave -- a wave for metal prices declining, you’re probably better off to own the metal than the companies, because the companies tend to underperform the metals in a bear market. Bear markets feed on themselves. So if an investor is losing money, he’s not going to want to buy another speculative gold company or copper company. So it’s true that even in bad, bad markets, you will have some great investment successes where a company has had good exploration results or has done a really, really smart acquisition. You will have those. But typically the whole sector is going to be losing out and the best strategy then is to do what nobody does which is sell at the top. Buy at the bottom, sell at the top. That’s what you’re supposed to do. But of course nobody ever does that. It’s times like this where we’ve had four years of bear markets and I don’t know whether the bear is going to turn into a bull market in a year or two years or two days. I really don’t know when the bottom is. But I know this is not the top. We’ve had four years of terrible markets. I would say today is just a really good time to be building a portfolio of well-run junior companies. My bias is in gold because I think that gold and silver are going to outperform the other metals. But buy a portfolio of companies and really focus on a couple of things. One is the asset has to be good. You can have a genius with a crappy asset and he’s not going to make money. You can have an idiot with a phenomenal world class asset and he’s actually going to make money. The stock is going to go up. The second thing is: people are really, really important. But my first priority is to look at the asset, to look at the quality of the project that the company has............there are a lot of similarities today to what typically happens in the bottom of the bear market. There is a lot of sadness, a lot of difficulty raising money, a lot of very stressed junior companies, and very unhappy investors. That’s the nature of the beast. When things turn, the tide will come in and everybody will be happy again.

The major mining companies are decreasing their costs, but what they’re really doing is increasing their future costs. They’re pushing costs out into the future. That has to be resolved but my sense is that we are in a bottoming process. I don’t think it’s going to get a lot worse and I think that two or three years out, these major mining companies are going to wake up to the fact that they’ve shut down exploration. They’ve shut down their development. They’ve got nothing in the pipeline and all of a sudden when they’re announcing their costs the analysts will start saying, “Yeah, but you don’t have any more ore.”So you want to identify the properties and the people that can last through this bottoming period, as well as those companies that will come out the other end in possession of the very few quality discoveries that are out there. That’s all you’ve got to do—simple, right? Haha......There are probably six gold projects in the world right now that are being developed that I think will probably work, held by junior companies. I’m not talking about majors.In terms of companies that are competent, we’ve got something like 1500 listed on the Vancouver exchange. I would say probably – 20% percent of them are companies that I would consider putting money into [in the right circumstance]......Maybe 25%. But I don’t buy everything. My portfolio, I try and keep it to 20 companies or less and I think that’s something investors should do as well. If you own too many stocks, you forget why you bought them. They go up, they go down…and then you start hoping they go back up for no reason at all. That’s my philosophy anyway.

It is really quite amazing that we chucked billions and billions and got no supply response at all. What this tells us is that there is simply not a lot of gold out there. How many genuine finds were there in the last cycle? Half a dozen? A dozen? In fifteen years we might have discovered enough new material to keep the mills turning for two or three years. The raw material was just not there, even in the face of the avalanche of money to tease it out.......... To step back and re-cap: being an asset class unto itself which from time to time comes into favour generates substantial investment demand. Gold is a small sector to begin with – lots of money into a small sector drives down the cost of capital and encourages issuance. Against this there are fewer still opportunities within the small sector to invest the incoming capitalThis leads to gross misallocation of capital as the financial sector chases scale, growth and leveraged returns in marginal projects. As Saville discusses elsewhere buying low value ounces in the ground was once a successful strategy, but not now. As Rick Rule has discussed this leaves a marginal industry as prices fall.

Mr Mehta would not name the Australian mines nor companies that he was looking at, but said talks with advisers had begun. "We have met a lot of investment bankers here and we are evaluating the best way to get in, what is the best way to do it, as we are looking at not only taking interest in the gold mining sector but we are also looking at forging a relationship with the largest gold-producing mines to buy and ensure supply from them," he said. "We can be a good consuming partner for them." The comments follow recent momentum towards a free trade agreement between Australia and India, and last year's visit to Australia by Indian Prime Minister Narendra Modi. It also comes after two years of regular deal-making in the Australian gold industry, as several foreign gold miners have sold assets to try to reduce their exposure to Australia.

Cipher Research has developed a new, simple, and powerful tool to analyze profitability, the Adequacy Ratio (AR). It is cash inflows (revenues) divided by cash outflows (OP-EX + IMP + debt repayment + dividends paid). Note it does not include equity raises or cash spent on acquisitions. If the ratio is greater than 1.0 a company is healthy; if less than 1.0, unhealthy. Of the seven companies we looked at over 11 years, none had an average ratio greater than 1.0 over the period. Only for one year, in 2011 when gold hit its all-time high, did the average adequacy ratio for the companies as a whole exceed 1.0. To compare for example, Apple has a 1.3 adequacy ratio over the past 5 years.This industry-wide failure means the major gold miners have not generated enough cash flow to meet their obligations despite the amazing 11-year run for gold. We found that companies have been going into debt to pay dividends. For example, Newmont took on an additional $5.8 billion in debt and paid out $5.2 billion in dividends over the period. We know of small-tier junior miners that have paid out dividends with equity raises… that’s unholy and in my opinion, should be illegal.

.......It feels as if the markets are programmed to crash when the ECB's QE programme nears its end, if not before.Pettis on Debt restructuring

As soon as Draghi made the statement to do “whatever it takes”, markets recognized that the ECB was in effect guaranteeing the bonds of EU member states whose credibility was in question, and yields immediately dropped. It is important to understand why this was effectively a kind of debt restructuring. .......Draghi’s promised immediately reduced a larger part of the uncertainty associated with the resolution of the debt. The collapse in uncertainty reversed the reflexive process in which rising uncertainty caused declining economic expectations, which caused rising uncertainty.

Franco-Nevada Corp., a Canadian company that provides financing for energy and mining projects, sees sagging commodity prices as an opportunity to complete deals worth more than $1 billion this year.

“I’d like to deploy all my cash this year,” David Harquail, chief executive officer of the Toronto-based company, said in an interview in Vancouver Monday. “That would be my ideal.” Harquail, who put more than $900 million to work in 2014, said mining and energy companies need more financing for projects hurt by falling prices. Franco-Nevada and other buyers of royalties provide financing to developers in exchange for a discount on future output.

Baker Steel (additional link HERE) looking to increase assets 6 fold by $180mEMR Chief Executive Jason Chang said the fund will focus on copper, gold, coking coal and the fertiliser potash, and had attracted a mix of institutions, endowments and private investors....."We think now is a good time to deploy capital into these markets," Chang told Reuters in an interview. "We're looking at the medium to long term and not worried about the day-to-day fluctuations."

The Baker Steel Resources Trust – which has lost nearly three quarters of investors’ money – is asking for clients to pile in millions more in an audacious call that the commodity slump will soon be over.The investment trust, managed by David Baker and Trevor Steel, has lost investors 72.3 per cent in the past three years, according to FE Analytics.Investors have been fleeing from anything related to commodities in the belief that the ‘super cycle’ sparked by China’s rapid growth had come to an end.The £31.4m trust is planning to increase its assets sixfold through a £79m share issuance and a further £100m capital raising to be outlined at an extraordinary general meeting later this month.

While he admitted it was impossible to call the exact bottom, he said with valuations as low as had been seen in many years, much of the “smart money” in the private equity space was also poised. “We are at or somewhere near the bottom,” he said. “Whether we have actually seen it or whether we will in another six or 12 months, I don’t know. But the risk-reward of the potential upside looks positive.” He thought the current conditions would not “last forever”. “The sector is on its knees and we would like more capital to take advantage of that. Mr Steel said with the new money he would be interested in adding a handful of development-oriented stocks, of which he had already identified a pipeline of potential names.

“There is very little competition in our space and it gives us an opportunity to do attractive deals,” he said. “It might be companies that need the last bit of capital to get their projects into production, or if they have a lot of debt. We can get involved in refinancing that debt – effectively exploiting that weakness – and getting in at a good entry point for our investors.” He said that while the sector could continue to fall, he wanted to raise the money now because the risk of waiting to get the deals done at a better price was too great.